Today’s letter is brought to you by Sidebar!

Ready to take your career to the next level? Make your transition successful by leveraging a Personal Board of Directors. A trusted peer group, with battle-tested perspective, and proven playbooks, to have real, tactical discussions with to propel you forward.

With Sidebar, senior leaders are matched with a small group of highly-vetted, private, and supportive peers to lean on for unbiased opinions, diverse perspectives, and raw feedback. Everyone has their own zone of genius. Together, we’re better prepared to navigate professional pitfalls and push each other to do more, do it better, and do it faster.

“Providing and receiving support from others who play a similar role to you is one of the best ways to grow your capabilities and succeed.” - Vice President, Roku

“You’re the average of the people you keep closest; Sidebar helps you raise that bar.” - Global Director, Reddit

“Tap into a new level of coaching support, professional development, and peer-driven accountability.” - Senior Director, Credit Karma

Why spend a decade finding your people – join Sidebar today. Join the growing waitlist of over 5,000 top senior leaders, and apply to become a founding member.

To investors,

Federal Reserve officials are now saying the quiet part out loud—they intend to keep interest rates high for an extended period of time.

This strategy is in-line with the central bank’s commitment to get inflation in the US economy under control. After manipulating the cost of money to 0% for years, the Fed had to reverse course at a record pace. The rise in interest rates from 0% to 5.25% happened at a pace that was never seen before, yet the estimated damage to GDP growth and the labor market never materialized.

The economy is still growing and unemployment is under 4%.

But consumers are now realizing that a long-term shift has happened in the economy. Originally, many citizens planned to wait out the Fed’s interest rate hikes. They thought they could buy a home or car next year. They could use their savings built up during the pandemic to outlast any negative wage growth. And they saw increased interest rates as a way to drive a little extra income from holding bonds.

The problem is that the Fed has been in demand destruction mode for almost two years now and yesterday’s press conference signaled a long-term commitment to keeping rates high.

This means the American consumer has a choice. They can continue to put their life on hold for a few more years or they can throw their hands up and subject themselves to more expensive capital.

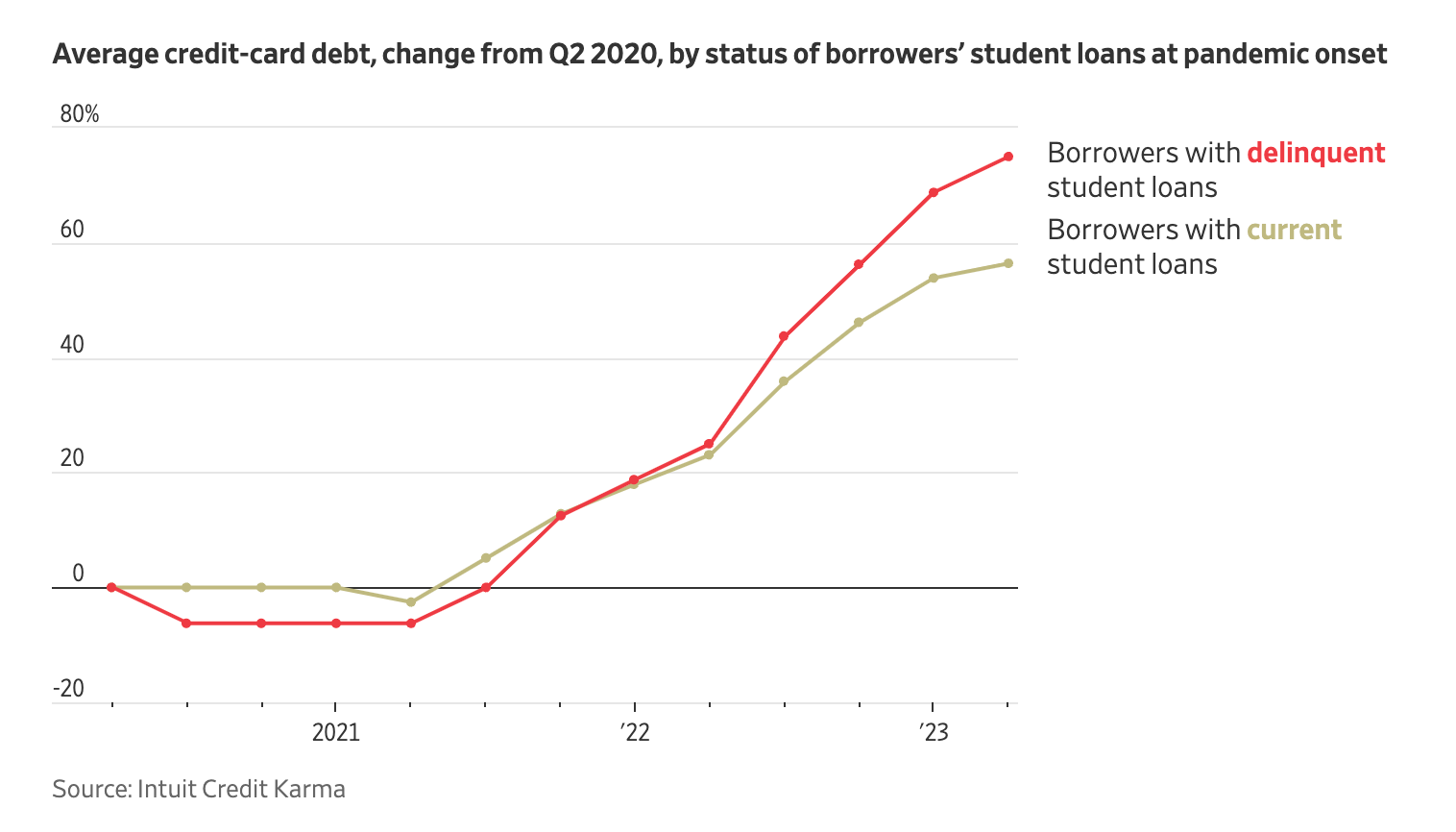

As Gina Heeb pointed out in the Wall Street Journal this morning, consumers are spending more of their income to cover housing costs, being forced to pay more on their car loans, and their credit card debt is exploding higher.

Based on this data, it appears that consumers are finally starting to live their lives and deal with the cost of capital increase. This makes sense from a psychology standpoint. It wouldn’t be too difficult to convince someone to put off the purchase of a home or car for a few months, but once you begin to talk about years, people don’t have the patience.

The average cost of a home, a mortgage payment, a car loan payment, and other ordinary living expenses will continue to rise nationally as rates remain persistently higher than they have been for the last decade.

The interesting part is that current interest rates are not necessarily higher than the historical average, but there is an entire generation of millennials who have spent their adult lives in a low interest rate environment. It had become the new normal. Every investment decision was based on an assumption of low interest rates. So was every purchase decision.

Now that rates are higher, and the Fed is signaling a commitment to long-term higher rates, this generation of consumers and investors will have to recalibrate. The irony of the situation is that boomers were slow to acclimate to low interest rates because it was foreign to their lived experience, but now millennials are likely going to be the ones who are slow to acclimate to high interest rates.

There is no specific cure to the problem. The pain will continue until young people realize the world has changed and they now live in a new regime. Their investment decisions now have to account for 5% interest rates. Their car and mortgage payments are going to be higher than they anticipated.

But that is the price for living today. It may not seem fair, but the worst mistake would be sitting around complaining rather than living life. Time is the most finite resource we get. Letting the central bank steal it from you because they made capital expensive sounds like a bad plan.

It won’t be easy for many people to figure it out, especially because we are talking about income and rising expenses, but it is possible. And all we can ask for is a chance to live an extraordinary life that makes us happy.

Hope you all have a great day. I’ll talk to everyone tomorrow.

-Pomp

Paolo Ardoino is the CTO of Tether. In this conversation, we talk about the rise of stablecoins, whether the market is winner-take-all or not, treasury management, how they ensure the peg stays actually backed by dollars, regulation & audits, accumulating bitcoin, banks, FDIC insurance, and more.

Listen on iTunes: Click here

Listen on Spotify: Click here

Earn Bitcoin by listening on Fountain: Click here

Tether Co-Founder Explains Reserve Strategy

Podcast Sponsors

Trust & Will - Estate planning made easy. They are fast, secure, and simple to use. Get your will or trust created today.

Auradine - A new bitcoin miner powered by the world’s first 4 nanometer silicon chip technology.

Velo Data: Do you want faster, easier crypto data? Sign up for Velo Data, a new product that we have been working on to solve this problem.

You are receiving The Pomp Letter because you either signed up or you attended one of the events that I spoke at. Feel free to unsubscribe if you aren’t finding this valuable. Nothing in this email is intended to serve as financial advice. Do your own research.

Share this post