Today’s letter is brought to you by Cal.com!

What do I have in common with Chad Hurley (YouTube), Tobi Lütke (Shopify), and Alexis (776/Reddit)?

We are all early investors in Cal.com and we use it instead of Calendly. Cal.com is the leading open-source scheduling platform, which gives you the same superpowers of efficiency previously reserved for elite corporations and tech gurus.

Stop wasting your time with scheduling software that doesn’t work. Use technology to make your life easier.

Cal.com is transforming sophisticated calendar management into an accessible tool for all via a user-friendly interface. Set up is quick, easy, and you will never go back to your boring calendar tool.

Exclusive for Pomp Letter subscribers, use code “POMP” for $500 off when you set your team up with Cal.com. Save time. Save money. Use Cal.com.

To investors,

After an explosion in asset prices and inflation in 2020-2021, the Federal Reserve has remained committed to destroying demand and getting the economy under control. The fastest interest rate hikes in history since March 2022 had the desired effect of destroying investment demand.

We saw the S&P 500 drop more than 20% from the peak of Q4 2021. TLT, the 20 Plus Year Treasury Bond ETF, is down more than 12% in the last 12 months.

But seeing investment values fall significantly is only one part of the equation. Citizens have three options with their money — they can invest it, they can spend it, or they can save it.

If the Fed is able to discourage people from investing, they still need to discourage people from spending the money if they want to succeed in their fight against a hot economy. The data from Black Friday suggests that the consumer may not be listening to the Fed nearly as much as the central bank would like.

Rebecca Picciotto writes for CNBC:

“Black Friday e-commerce spending popped 7.5% from a year earlier, reaching a record $9.8 billion in the U.S., according to an Adobe Analytics report, a further indication that price-conscious consumers want to spend on the best deals and are hunting for those deals online…

… [Vivek] Pandya noted that impulse purchases may have played a role in the Black Friday growth since $5.3 billion of the online sales came from mobile shopping. He noted that influencers and social media advertising have made it easier for consumers to get comfortable spending on their mobile devices.”

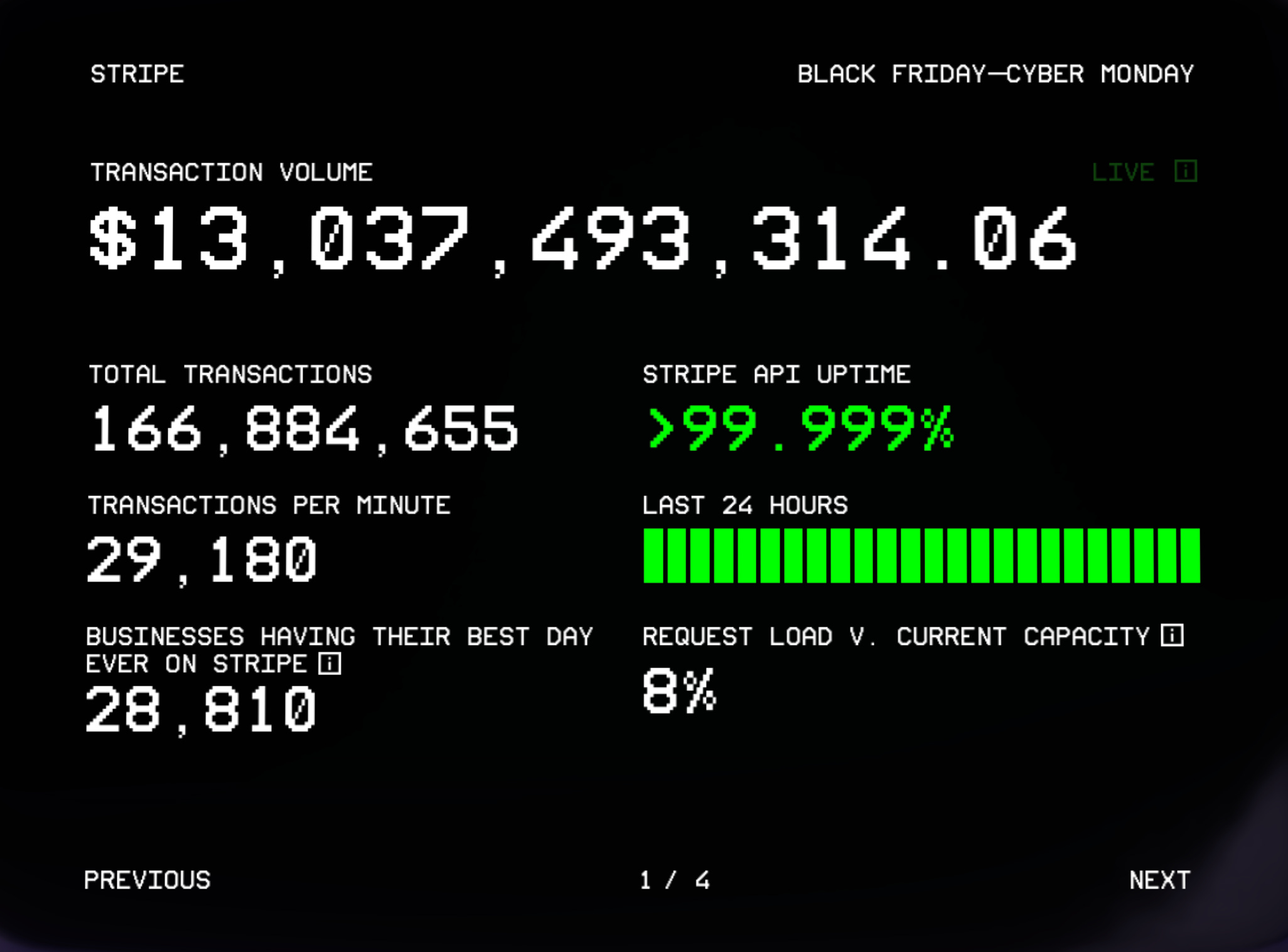

These are very large numbers. Stripe, the fast-growing payments company, built a live dashboard to track various metrics for Black Friday & Cyber Monday. As of 8:30am EST this morning, the dashboard showed more than 166 million transactions and $13 billion in transaction volume.

These numbers are exclusively for Stripe, so you can imagine how much larger the numbers get when you incorporate all payment processors. Unfortunately we won’t have that data for a few more days.

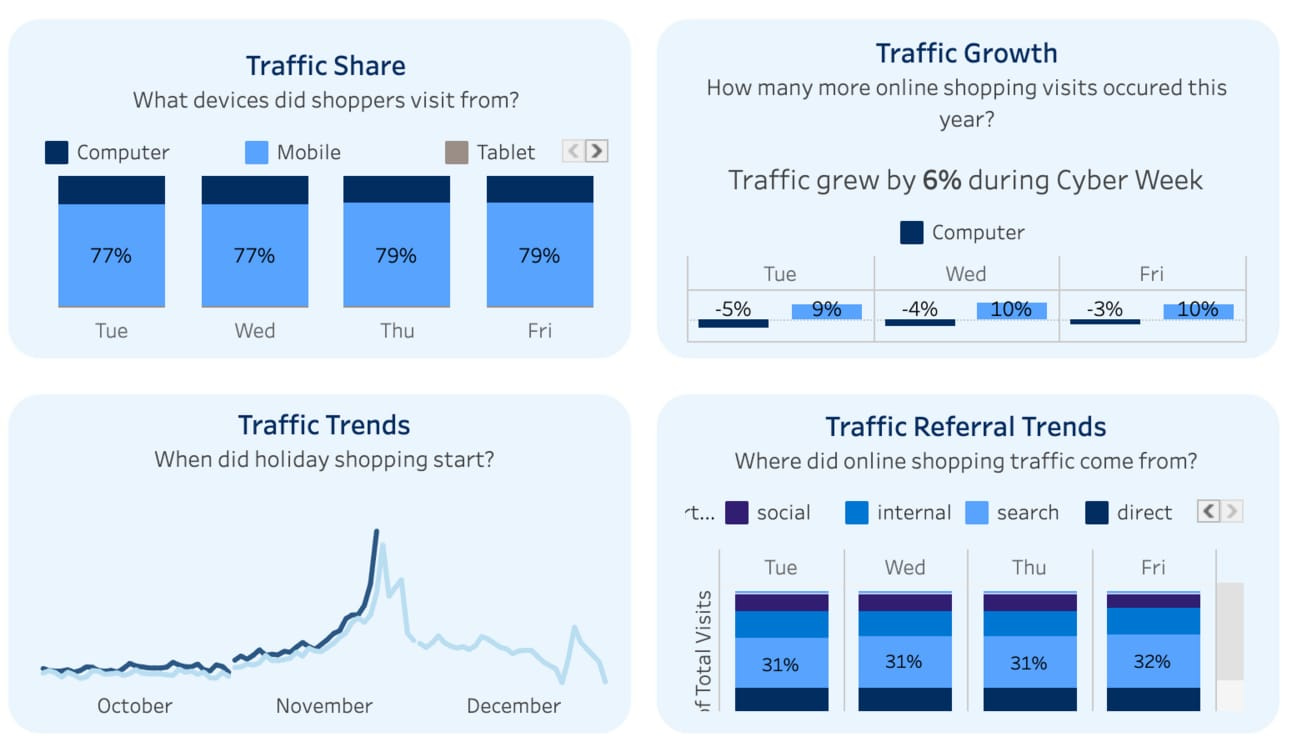

Another interesting data point from Salesforce that was highlighted by Bay Area Times, and supports Pandya’s analysis of impulse purchases, is that 79% of all purchases came from mobile, rather than the majority being driven by desktop users.

So what does this have to do with the Federal Reserve and inflation? While the central bank has been successful in destroying investor demand, they seem to have failed at destroying consumer demand so far.

That doesn’t mean they will not be successful in the future, but so far the data is overwhelming in proving that consumers are still ready to spend money on consumption.

An important question to ask is where all this money is coming from that the consumer is spending. According to the New York Fed, the Q3 data shows that households continue to take on more debt across various debt types.

“Total household debt rose by 1.3 percent to reach $17.29 trillion in the third quarter of 2023, according to the latest Quarterly Report on Household Debt and Credit. Mortgage balances increased to $12.14 trillion, credit card balances to $1.08 trillion, and student loan balances to $1.6 trillion. Auto loan balances increased to $1.6 trillion, continuing the upward trajectory seen since 2011.”

Matt Egan explained for CNN why this rising debt situation, especially for consumer credit cards, is important to pay attention to:

“In 2022, about one in 10 (9.9%) general purpose credit card accounts in the United States were in “persistent debt” — a difficult-to-escape situation where borrowers are charged more in interest and fees than they pay down in principal, according to a new Consumer Financial Protection Bureau report shared first with CNN.

That’s up from 8.4% in 2021, a trend that the CFPB blames on shrinking paychecks (after adjusting for inflation) and rising borrowing costs.”

To make matters worse, Egan continues:

“Americans were hit with $105 billion in credit card interest last year alone, according to the CFPB’s biennial consumer credit card report. That includes $30.5 billion in the fourth quarter, the highest since at least 2015.”

The problem is only going to get worse unfortunately. Interest rates on credit cards have been spiking in a fairly insane manner. The average interest rate on all credit card accounts in the US is now over 21%. Just look at this chart from LendingTree showing historical credit card interest rates:

Not exactly what you want to see if the American consumer is using credit card debt to continue to spend enormous amounts of money on consumptive goods.

So we have an economy that is still showing a strong consumer spending pattern, but it appears to be financed increasingly with debt. Where else have we seen this happen? The US government. Spending from the federal government has continued to increase, along with more and more borrowing. We are turning into a nation of borrowers. There is no fiscal discipline at the government or individual level on average.

There is still time to turn around both ships, but the probability gets lower with each passing day. Never bet against America. But America better hurry up and get back into strong financial shape, so we are prepared to deal with a recession if it ever comes.

Hope you all have a great day. I”ll talk to everyone tomorrow.

-Anthony Pompliano

If you enjoyed this letter, you should consider subscribing to the Pomp Letter. I write 3-5x per week and explain in simple language what is happening in the economy, financial markets, and bitcoin.

Cliff Weitzman is the founder & CEO at Speechify.

In this conversation, we talk about the explosion in audio content on the internet, how text to speech audio has become so great, why exactly so many people are now listening vs reading or watching, and how this impacts content creators and human productivity.

Listen on iTunes: Click here

Listen on Spotify: Click here

Earn Bitcoin by listening on Fountain: Click here

This Immigrant Helped 25 Million Read With Artificial Intelligence

Podcast Sponsors

Cal.com - Changing the calendar management game. Use code “POMP” for $500 off when you sign up.

Trust & Will - Estate planning made easy. They are fast, secure, and simple to use. Get your will or trust created today.

Auradine - A new bitcoin miner powered by the world’s first 4 nanometer silicon chip technology.

Base: Base is shaping the future of the on-chain world with near-zero gas fees and rapid transaction speeds.

ResiClub: Your data-driven gateway to the US housing market.

Bay Area Times: A visual newsletter explaining the latest tech & business news.

You are receiving The Pomp Letter because you either signed up or you attended one of the events that I spoke at. Feel free to unsubscribe if you aren’t finding this valuable. Nothing in this email is intended to serve as financial advice. Do your own research.

Share this post